Tokenized Real Estate is here. Are You Ready?

Since every piece of real estate is unique, NFTs / Smart Contracts could be a great way to represent them. If a token represents a property, you have digital proof of ownership in your digital wallet. That can be plugged into another smart contract to help with the following:

- Mortgage / Refinance — it can take months to secure a typical mortgage, requiring all sorts of documentation and + a good credit score. If you have a token to represent a property, that can be used as collateral to get a loan. In DeFi, you can get a loan in seconds if you have the collateral to back it.

- Invest anywhere in the world — people can pool capital together to invest in specific properties, not limited by geographies, and invest with small amounts of capital.

- Price and title history of a property — once a home’s info is on the blockchain, any transfers in title or ownership are publicly available, getting rid of the need for title insurance over time and providing price transparency on previous sales of the home

- Trade properties entirely online — instead of working with traditional brokers and paying 6% in commissions for each sale, imagine being able to sell your property NFT on a marketplace and have the transfer of ownership happen entirely online.

Tokenizing real estate is complex — not only is there technical complexity to setting up the contracts — but you need to register the token as a security with high costs. When considering the possibilities, people often ignore that many of these features haven’t been built out yet due to the current restrictive policies established by the SEC and the local governments where the property resides. To help adopt tokenized real estate, we want to lay out some of the legal and regulatory frameworks that you will need to navigate if you're going to tokenize real estate.

Regulatory Environment Around Real Estate Tokenization

When tokenizing a property, ask yourself what to do with it. If you plan to sell it in the open market or to a subset of investors, the use case likely passes the Howey Test. If it does, you need to register the property as a security. Under the Howey Test, a transaction is an investment contract if:

- It is an investment of money.

- There is an expectation of profits from the investment.

- The investment of money is in a joint enterprise.

- Any profit comes from the efforts of a promoter or third party.

A few companies today are fractionalizing real estate via tokens or NFTs that pass the Howey Test but are not registering the offering as a security. That’s scary for a few reasons. As a founder, or a person selling tokenized real estate but not registering it as a security, you may be committing investment fraud whether you realize it or not. Selling unregistered securities is considered a felony by the SEC and opens you up to legal action from those who purchase the tokens you sell. This applies to the general NFT space as well. We’re beginning to see the SEC more actively involved in the NFT space with their recent action against the former PM at Opensea, who was charged with committing “insider trading” for buying up NFTs ahead of them being featured on Opensea’s front page.

Okay, your real estate token offering passes the Howey Test; what are your options? Luckily, private placement options exist, so you don’t need to offer public security.

Let’s explore the options available.

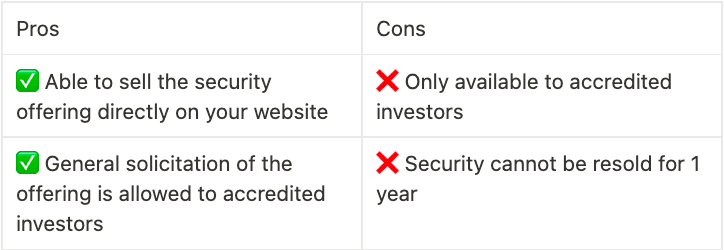

Private Security Offerings (Security Token Offerings) Options:Regulation D Offering

Regulation D provides two significant exemptions from registration for some offerings.

Under Rule 504 of Regulation D, a company can offer and sell its virtual tokens to unlimited investors, but the offering is limited to only $5 million during any 12 months.

Rule 506(b) permits sales to up to 35 purchasers who do not qualify as accredited investors but prohibits general solicitation. Rule 506(c) requires that all purchasers qualify as accredited investors but permits general solicitation. In comparison, under Rule 506, a company can offer and sell unlimited virtual tokens.

Regardless of which rule is used to exempt an offer of virtual tokens under Regulation D, the tokens will be subject to transfer restrictions. Those restrictions generally prohibit the tokens from being resold or transferred for at least one year after purchase.

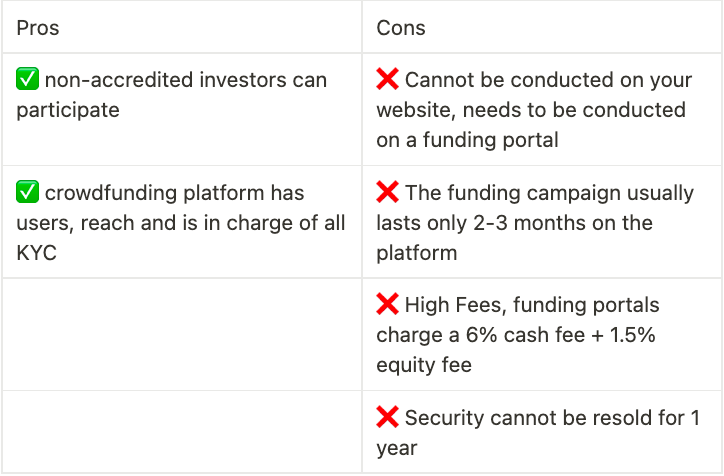

Regulation CF Offering

The most commonly used exemption for tokenizing real estate is Regulation CF Offering. This exemption allows a company to raise $5M million through crowdfunding offerings in 12 months.

Regulations CF creates a streamlined registration process for smaller real estate developers, operators, and funds to experiment with real estate tokenization and secondary market trading of tokenized securities—the set-up process for launching a tokenized real estate Reg. CF offering could take as little as 5–6 weeks.

Real Estate companies can use Regulation Crowdfunding to offer and sell tokenized real estate securities to the investing public allowing the public to participate in the early capital-raising activities of early-stage real estate projects.

Anyone can invest in a Regulation Crowdfunding offering, including unaccredited retail investors, and the offering must be listed on a crowdfunding platform.

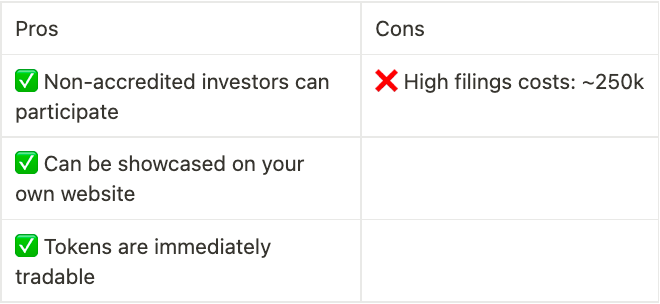

Regulation A+ Offering

Requirements for Reg A+ offerings are relaxed compared to a registered IPO. Still, Reg A+ allows U.S. and Canadian companies to publicly advertise investment opportunities and raise $75 million in 12 months from unlimited unaccredited investors.

Also, this exemption provides immediate liquidity to investors, meaning that tokenized Reg. A+ securities can be traded on day 1 of issuance on regulated Alternative Trading Systems (ATS) in the US and overseas.

For these reasons, Reg A+ offering is often called a mini-IPO. Tokenized Reg A+ offering is an excellent fundraising tool for real estate developers, operators, startups, and existing companies.

After deciding which pathway to take, you will need to ensure that the standardized token offering is compliant, has a governance structure, and shares that can be traded on secondary markets called Alternative Trading System platforms in the US.

The Future of Tokenized Real Estate

Modernizing an industry operating as if it is still in the 1980s is difficult. Many incumbents are happy keeping the status quo since they currently benefit from the system. These companies are the title insurance companies, traditional banks that underwrite most property loans, and large institutions that benefit from siloed information on real estate. Not only that, but government institutions need to be faster to change their processes. For example, when purchasing a property, you must go to the county clerk’s office in person to transfer a property deed in many counties in the US.

The benefits of tokenizing real estate are clear: more liquidity, faster transactions, price transparency for homes, and online transactions. For crypto and DeFi to truly disrupt the real estate industry, it will be necessary for web3 companies to partner to push for broader adoption. It’s a question of whether companies can navigate the strict regulations to still create use cases for real estate that benefit from DeFi. That or current regulations must change to make real estate tokenization easier.

In the meantime, we’ll keep building towards democratizing access to real estate investing and driving greater adoption.